This little-noticed bond-market development could put many borrowers on edge

If the Treasury yield curve continues to steepen this year, it would make it harder for long-term borrowers to feel the full impact of any 2026 rate cut by the Fed

Last Updated: Feb. 6, 2026 at 4:01 p.m. ET

First Published: Feb. 6, 2026 at 2:50 p.m. ET

Developments in the Treasury market this year could blunt the impact that another Federal Reserve interest-rate cut might have on borrowers.Photo: MarketWatch photo illustration/iStockphoto

Referenced Symbols

Key Points

About This Summary

- Global yield curves are steepening due to concerns about growing fiscal stimulus.

- A persistently steeper Treasury curve means consumers and businesses may not fully benefit from another Fed rate cut when it comes to mortgages and long-term corporate loans.

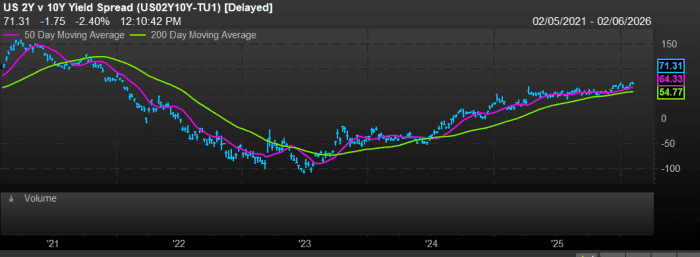

- The spread between 2- and 10-year Treasury yields sits near one of its widest levels in four years.

Big moves in stocks and cryptocurrencies have commanded the lion’s share of investors’ attention this week. But things are also unfolding in the bond market that could have major implications for borrowers this year.

A trading pattern known as a steepening of the Treasury yield curve gained momentum this week. If this dynamic remains in place by the time the Federal Reserve is ready to cut interest rates this year — or when traders solidify their expectations on the timing of such a move — it will likely be harder for consumers and businesses borrowing over a long-term horizon to enjoy the full benefits of lower short-term borrowing costs.

On Thursday, signs of a weakening U.S. labor market caused traders to boost their expectations for a Fed rate cut as soon as March and to price in a slightly greater chance of a total of three or more reductions by year-end. The policy-sensitive 2-year Treasury yield

fell at a faster pace than the rate on the 10-year note

as a result. That pushed the spread between the yields on the two notes to one of its widest levels in four years, at 72.8 basis points.

Why stocks in Europe and Japan are poised for more gains in 2026 See All Videos

The spread between 2- and 10-year Treasurys touched one of its widest levels in four years on Thursday.

Generally speaking, a steepening curve is often associated with a brighter U.S. economic outlook and an environment in which banks are encouraged to lend more freely because they can also borrow more cheaply.

This time around, though, something a bit different is going on. Yield curves are steepening around the world — including in Japan, Germany, the U.K. and Canada — because of a sense that “governments are adding to fiscal stimulus and concerns are growing around the sustainability of that,” according to Tom Nakamura, head of fixed income and currencies at AGF Investments in Toronto.

In the U.S., the Treasury curve has more room to steepen relative to bond markets in other countries for a number of reasons, Nakamura said in a phone interview on Friday. Those reasons include worries about an “overreaching” White House that may interfere with the Fed’s independence and push for lower interest rates, which could then result in inflationary pressures and investors demanding more compensation for the risk of holding long-term Treasurys, he said.

A Treasury curve that remains steeper around the same time the Fed is ready, or expected, to cut rates translates into a more difficult time for consumers or businesses looking for mortgages or long-term loans. Under that scenario, loans priced off of 10- and 30-year yields

would not be moving down in lockstep with the Fed’s rate move.

Officials at the central bank kept rates unchanged in January and have indicated that only one rate cut is likely to be appropriate for this year. Meanwhile, the central bank has purchased more than $90 billion of Treasury bills since December, which some say is helping to stabilize long-term borrowing costs.

A steeper curve “makes it harder to get by on those things that matter to consumers,” Nakamura said. “Even if the Fed lowers policy rates to stimulate the economy, borrowers may not get as much benefit from this on new mortgages or even with auto financing, which covers two- to five-year periods.” Meanwhile, companies looking to finance over a 10-year period or more would find the cost of doing so to be more expensive, he added.

On Friday, financial markets recovered from what has been a bruising week stemming from jitters over artificial-intelligence spending, along with tumult in bitcoin and metals. All three major U.S. stock indexes

closed sharply higher, with the Dow Jones Industrial Average crossing the 50,000 mark for the first time, and short-term U.S. government debt sold off slightly as investors embraced riskier assets.

The 2-year yield finished up by 1.2 basis points at 3.49%, while the 10-year rate remained near 4.21%. The spread between the two shrank to 71.2 basis points on Friday, a touch narrower than in the previous session.

Debt concerns “are not going away” and, if they persist, may leave the Treasury market “biased toward a steeper curve,” Nakamura said. But if the labor market falters in a way that raises expectations for weaker economic growth and softer inflation, this could flatten the curve around the time the Fed starts cutting rates. A flatter curve, he said, also has the potential to “offset fiscal concerns.”

About the Author

Vivien Lou Chen is a Markets Reporter for MarketWatch. You can follow her on Twitter @vivienlouchen.

View this MarketWatch article CLICK HERE

Leave a comment